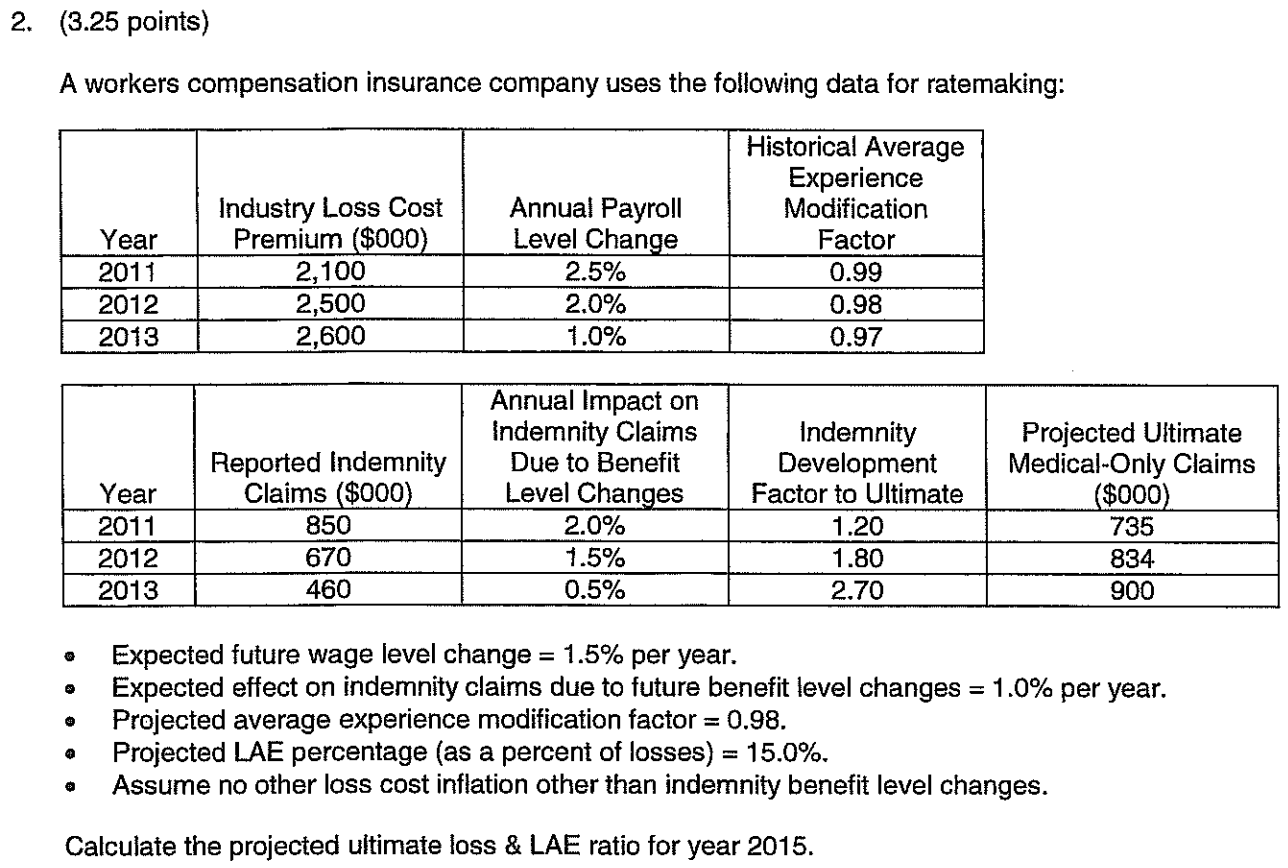

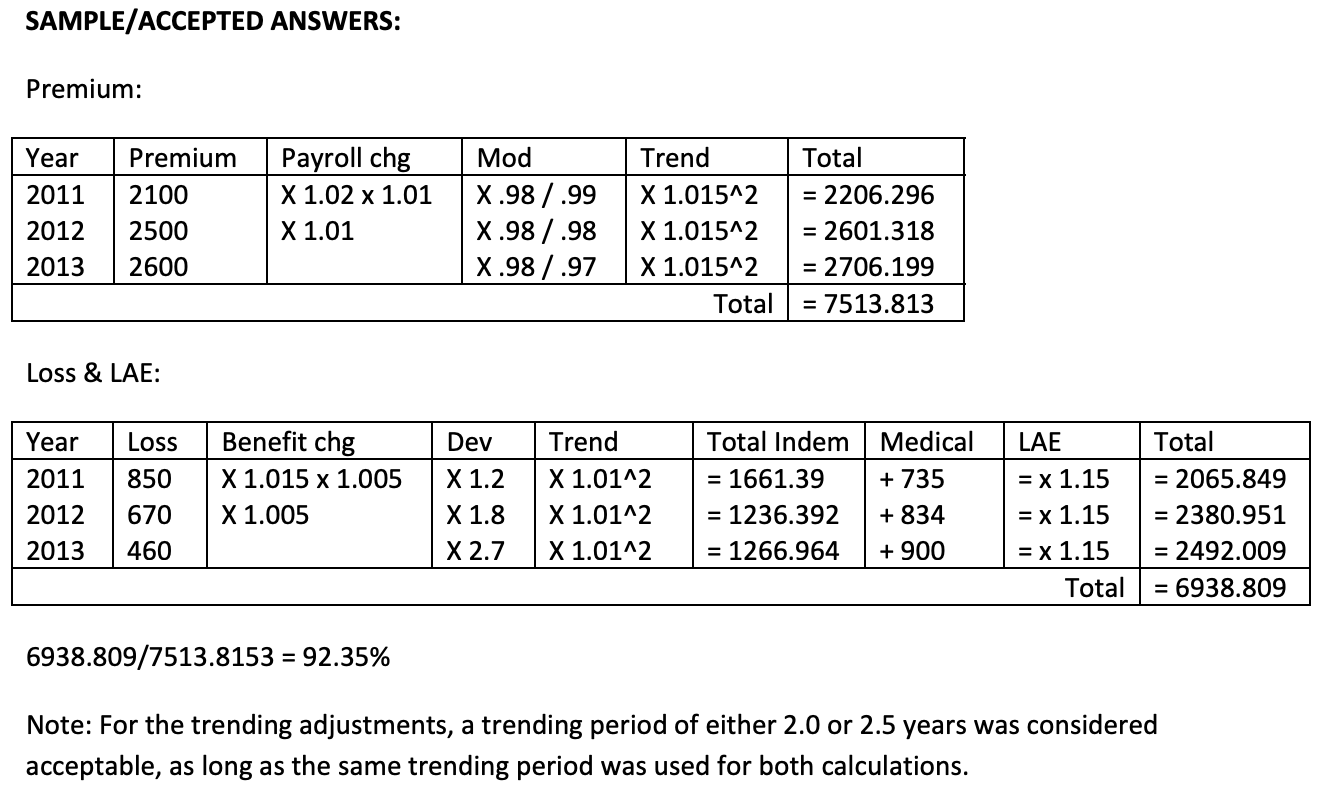

Spring 2014 Q2

in WernerD.WC

What is the average experience modification factor an why is the mod adjustment done in that way in the solution?

Comments

The average experience modification factor can be calculated by taking the average of the provided factors over the years.

From the data provided:

Average Experience Modification Factor = (0.99 + 0.98 + 0.97) / 3 = 2.94 / 3 = 0.98

As for the mod adjustment in the solution, the modification factor is applied as a multiplier to the premium to adjust for the individual experience of the employer compared to the average employer in the industry. If the experience modification factor is less than 1.0, it indicates that the employer's loss experience is better than average, leading to a decrease in premium. Conversely, if it's above 1.0, the employer's loss experience is worse than average, leading to an increase in premium.

In the sample calculations: For 2011:

Here, the premium is being adjusted by the experience modification factor, which acts as a discount or surcharge based on the employer's historical loss experience compared to the industry average. The formula given multiplies the premium by the mod factor, effectively adjusting the premium based on this experience. It's a common practice in insurance underwriting to reward or penalize policyholders based on their risk profile compared to industry standards.

"If the experience modification factor is less than 1.0, it indicates that the employer's loss experience is better than average, leading to a decrease in premium. Conversely, if it's above 1.0, the employer's loss experience is worse than average, leading to an increase in premium."

Could you further elaborate on this? If the loss experience is better than average, why would this lead to a decrease in premium? Is it because the insureds are less risky so they are charged a lower premium?

Yes, better loss experience means the insurer pays out less so using that data in the next rate indication means the rate need is less.