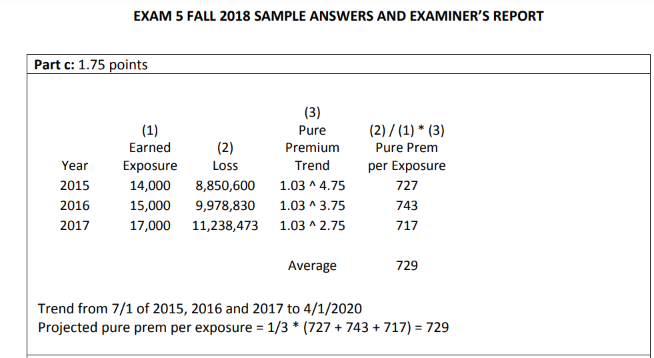

Fall 2018 Q7 c)

Hi, are exposures not also trended because pure premium is being trended, which includes the exposure trend? If the given trends were frequency and severity, would we apply those trends and the exposure trend?

It looks like you're new here. If you want to get involved, click one of these buttons!

Hi, are exposures not also trended because pure premium is being trended, which includes the exposure trend? If the given trends were frequency and severity, would we apply those trends and the exposure trend?

Comments

Wait.. applying frequency and severity trend is the same thing as applying pure premium trend. I guess my question then just becomes: why isn't exposure trend applied here?

If you were to apply the exposure trend to the exposures then you would need to apply that same trend to the losses so they trend would cancel out. (Unless there is a separate frequency and severity trend applied to the losses, the exposures and losses should move up and down together.)

The exposure trend would be used if you're asked to estimate how many exposures (i.e., policies) you'll have in the future, based on past data. In this case, you would apply the 3% annual increase to project the growth in the number of exposures.

For part (c), if you're calculating the projected pure premium per exposure using historical loss and exposure data, it seems that the goal is to find out the pure premium for the existing exposures rather than projecting new ones. Therefore, you wouldn't trend the exposures for past years because those are historical counts that are already known and fixed; they wouldn’t retrospectively change.