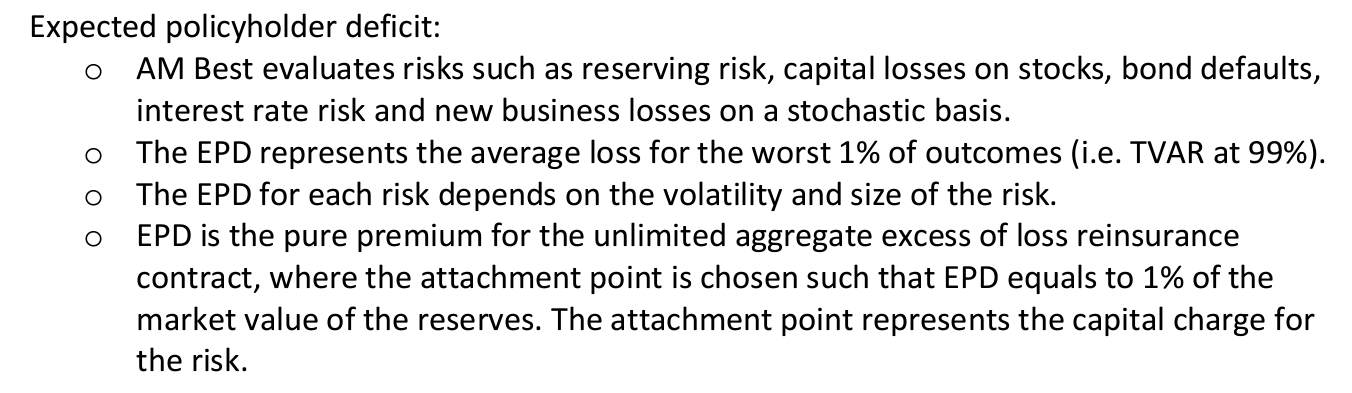

EPD (Expected PH Defecit)

Hi, may I know how should I link this to back to the BCAR? Or this has nothing to do with the BCAR.

I recalled that the 6 steps for AM Best Rate Process is BOB-ECL: BS Strength, Operating Performance, Business Profile, ERM, Comprehensive Adjustment and Lift/Drag.

And why is this using Pure Premium divided by Reserve, I don't really understand how this works. Can anyone help to elaborate a bit:

Thanks and Warm Regards,

Wilson

Comments

I'd say the BCAR is more related to the MCT whereas the Feldblum paper is more of interested in the "credit score" of the company if you will.

So for this, the 4th bullet point is trying to elaborate on the 2nd bullet. It's sufficient to just know the first 3 bullet points. No reason to unnecessarily confuse yourself with the 4th bullet.

EPD = TVAR at 99% = E[X| X > 99th percentile]

Thanks T1

Can we really say that EPD = TVaR @99%?

From what I understood, the EPD is a ratio and the BCAR capital requirement is set so the EPD is at 1%. So technically, EPD is "always" 1%. Am I talking non-sense? (I really might)

Yes, I think I sort of agree with you. When I read the paper, EPD is set such that the pure premium for an arbitrary aggregate XOL with attachment point X /reserves = 1%. It is not exactly TVAR. The source on page 18 also refers to TVAR and EPD as different things. Thoughts @graham ?

@Staff-T1:

So, just to make sure we're all looking at the same thing - it's the second bullet point quoted by @wilsonchan18 in the top post, which is copied from the examiners' report for part (c) of this question (2016-Spring Q22):

I agree that this is not correct. TVAR @ 99% is indeed the average loss for the worst 1% of outcomes as noted in this example from the Feldblum reading:

But this is not the same as having EPD = 1%. So the examiners' report looks to be in error here.

Even after reading this discussion, I am having trouble understanding what EPD at 1% means. Can someone explain this in laymen term?

Right now I have 2 conflicting interpretations:

1) EPD = $P / $V

$P is the pure premium for a reinsurance policy (unlimited aggregate excess of loss) to cover the expected value of loss given it’s the worst 1%.

The EPD in this case doesn’t have to be 1%, the only restriction in this calculation is to cover the expected value of the worst 1% ( E[X|X>99th percentile]

2) EPD = $P / $V

EPD has to be 1%, we just buy a reinsurance treaty such that this ratio has to be 1%

The second one doesn’t really make sense to me.

But the selection requirement is that we have to make EPD 1%.

SELECTION: choose required capital so that EPD = 1%

In this selection, what capital are we choosing?

But at the same time I don’t see how we can achieve both 1) and 2) at the same time.

1) As mentioned above, the EPD is the cost of buying an XOL insurance, P with attachment point Z that is at some level higher than your reserves, V. You'd find the value of Z such that EPD Ratio = P/V = 1%. It is not TVaR as the earlier poster rightfully pointed out. In other words, what XOL reinsurance with attachment point Z costs 0.01V.

2) The Capital amount that we are choosing is Z, the attachment point which represents a risk charge. On page 16 "For each risk, the capital charge $Z is set so that aggregate excess-of-loss reinsurance covering losses above an attachment point $Z has a pure premium equal to 1% of reserves."

I am still a bit confused, can you give me a simplified numeric example?

If you have reserves of 200M you have options to purchase XOL insurance where losses above a certain amount are covered by the contract. If you choose to purchase a 300M coverage for example, your premium could be 3M. A 400M coverage could cost 2M. In the case of the 400M coverage, your EPD or premium over reserves is 2M/200M, which is 1%. This would mean your capital charge Z is 400M.

I get it now thanks!