Calculation of LRC under PAA

In the source text there is this example

https://battleactsmain.ca/wiki6c/File:CIA.IFRS17-LRC_(065)PAA_LRC(5.2)_example_text1.png

_PAA_LRC_(5.2)_example_text1.png){kind=link}

Does this example provide enough information to figure out the value of derecognized assets or would they have to give us that amount in an exam question to calculate the LRC (excl. LC) at initial recognition?

In the formulas given, the acquisition expense components say "unless the entity chooses to recognise the payments as an expense" does this refer to the "non-directly attributable expenses"? So for example if there was $500 of acquisition expense but they "choose to recognize $100 as an expense" then there would be

- $400 of directly attributable acquisition expense and

- $100 of non-directly attributable acquisition expense?

Comments

Also, i don't recall any mention of it but i wanted to confirm if LRC can be negative?

Based on this description of the calculation at subsequent measurement in the IFRS17-LRC for the example linked above...

if i have a

Then LRC at end of year 1 consists of

is that correct?

and to go even one step further, the LRC excl. LC being negative has no bearing on whether the contract is onerous because onerousness is based on FCF > LRC excl LC?

Thanks, that's what is confusing me because conceptually i didn't think LRC could be < 0 but when i follow with the excel worksheet in the wiki for this problem

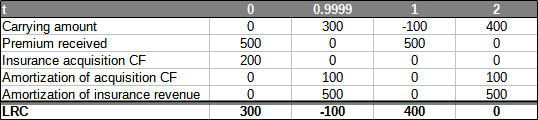

if i think about a 2 year policy like the above example with $500 paid each year and $200 of directly attributable acquisition expenses

then performing the calculation you would arrive at a negative number....

Based on the footnote of the source under the example

if insurance revenue represents the earned premium then insurance revenue must be $500 in the above example. So there's clearly something i'm missing for all the pieces the fit

How is your earned premium greater than your premiums paid at inception though? How can you have $1000 dollars of earned premium on $500 of written premium? I think that's the biggest issue here ~

I think he means right before receiving the second payment, like so:

Now that I think about it, maybe it makes sense? If the insured was to cancel right before paying the second payment, the company would get more back from the pre-paid acquisition expenses than they expect to pay for the remaining coverage of the paid premium, so liability is indeed negative

I just realized this whole hypothetical question doesn't work as it is not PAA eligible so there's nothing much to say here since it has to go under GMM

Oh yeah, you're totally right, for some reason I did not consider this at all! I checked and LRC does indeed stay positive for the whole duration using GMA under these assumptions

Thanks!

Thanks for the discussion! and for the screenshot of the table AnLaPe, that helped me understand it better (I guess i should have tried it out myself!)