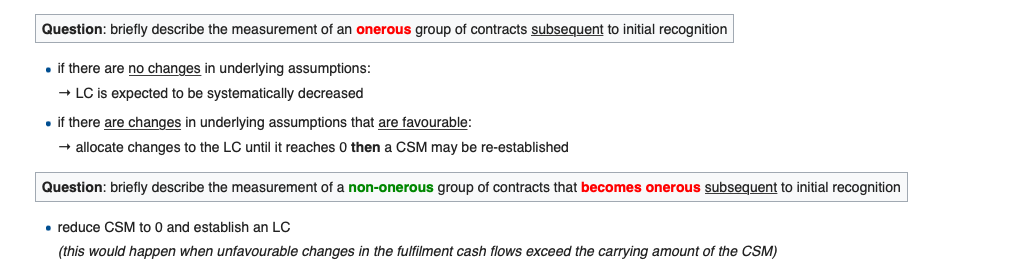

changes in CSM/LC subsequent to initial recognition

I understand the logic behind these 3 adjustments to the LC/CSM based on changes in underlying assumptions. What would happen in the remaining cases though?

If the onerous group becomes more onerous, would the LC be increased (or released less)?

If the non-onerous group becomes more profitable, would the CSM be increased (or released less)?

Or are these just going to be adjusted via the FCF?

Thanks!

Comments

If it is due to a change in facts and circumstances then: